Before closing on your home in Tennesse, check off this insurance guide to ensure you have the perfect coverage for any weather, floods, and peace of mind.

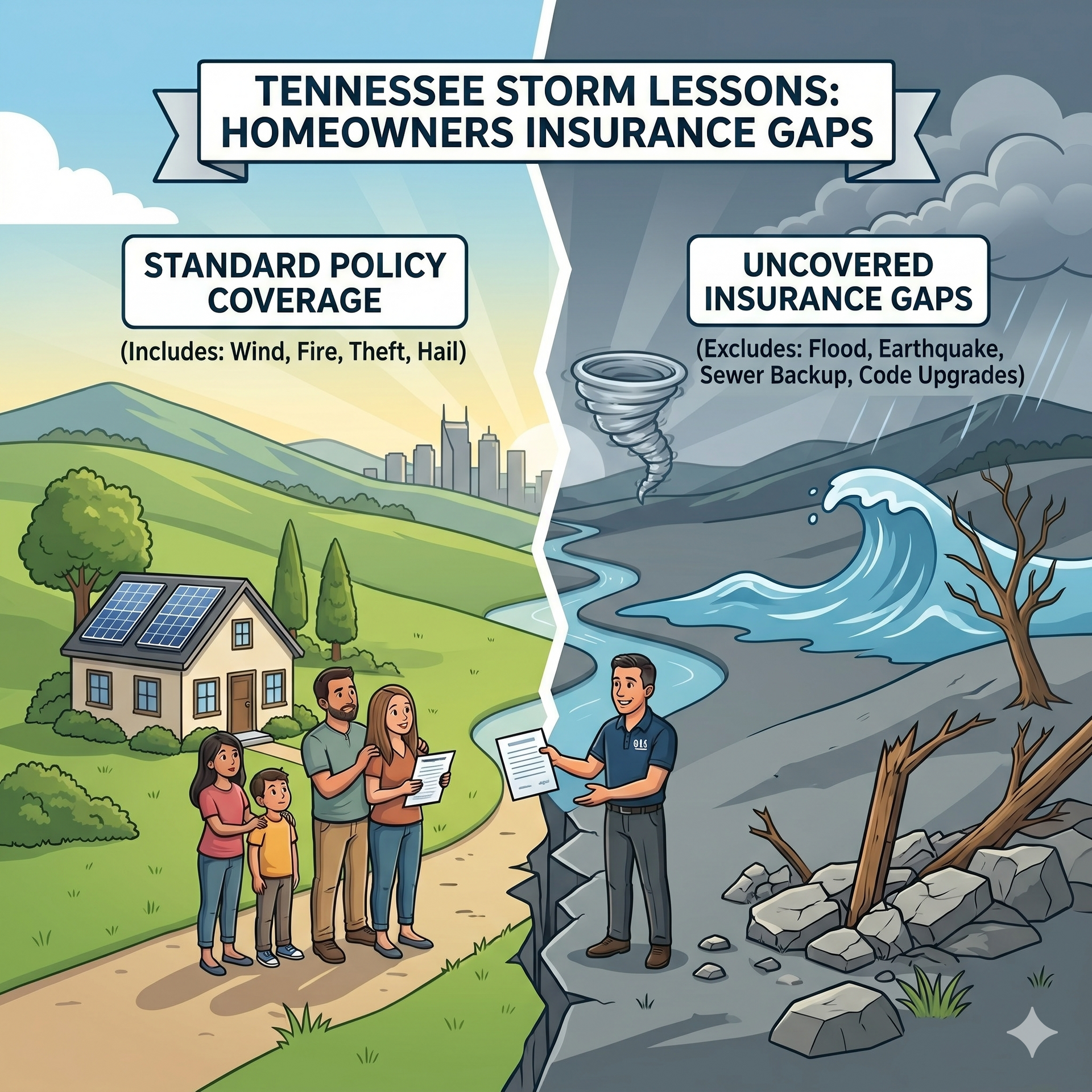

Learn about the homeowners insurance gaps that have been exposed by past TN storms. Review your coverage with us today for better protection!

Why are insurance rates higher in Nashville than Murfreesboro? We break down the 10 factors affecting your Middle Tennessee premiums. See how ZIP code impacts cost!

Discover what life insurance really is and why it’s vital for Tennessee families. Learn how to choose the right policy for your future with 615 Insurance Agency.

Understand Builders Risk Insurance for construction projects. Contact us for tailored coverage options today!

Own a historic home in Tennessee? Learn how to insure it right—protecting its charm, meeting preservation rules, and ensuring full coverage for restoration.

Are you driving in Tennessee? Learn what auto insurance coverages you really need to stay protected from accidents, storms, and uninsured drivers on TN roads.

Learn what Tennessee homeowners need to know about remodeling insurance, contractor coverage, and policy updates to protect your home investment the right way.

Understand the need for flood insurance in TN. Check your risk zone & get a quote today!

Uncover life insurance myths that can cost you. Get informed & secure your family's future with affordable coverage options today!

615 Insurance Agency Blog